The recent spread of the Coronavirus Disease (COVID-19) and required quarantine has caused many businesses to slow or close shop. This shutdown has caused widespread ripple effects throughout our economy resulting in the largest one-week increase in unemployment in our nation’s history, reaching over 1 million applicants, and in the U.S., there was over 3.2 million. Businesses that fall under the mandatory shutdown include self-employed individuals, small businesses, corporations and the gig economy and even those that remain open are affected in some fashion. The unfortunate fiscal effect of the COVID-19 pandemic comes at a time when everyone should be focused on staying safe and healthy rather than agonize about paying their bills.

The sudden economic fallout has led many individuals to call for a nationwide rent strike – a notion which is semi-supported by the Government who has mandated that banks should provide mortgage deferral payments to those affected by the virus. These measures are meant to assist homeowners and landlords, who rent out to tenants. Superficially, this seems to be a fair trade-off – if the landlord doesn’t pay the bank, then the tenant shouldn’t pay the landlord – yet many landlords are drawing a hard line in the sand about the requirement of rental payments; why is this?

What is a Mortgage Deferral?

To begin to understand why landlords have not been able to completely unwind rents we first need to explore the relief the banks are currently providing. They are offering a mortgage deferral for those affected by the crisis. The deferral is an agreement made between the mortgage borrower and lender. The agreement indicates that both parties have consented to suspend mortgage payments for a temporary length of time. The interest accrued due to skipped payments is added to the mortgage’s outstanding balance, and the additional interest is incorporated into future monthly payments once payments resume. In short, the borrower will need to repay the amounts during the skipped periods including both principal and interest, and inevitably increase the total amount owed compared to the original payment schedule. This is a stark difference from a mortgage payment abatement, which would allow for full forgiveness of missing a payment, or two, that could be passed down to residents.

As of now, the application process for relief is performed on a case by case basis. For individual homeowners, a simple questionnaire is employed: whether one’s employment status has been affected, if household income has been materially impacted, mortgagor’s information, and first and last name. The goal is to expedite the application process as quick as possible. However, for landlords, banks are only starting to iron out their processes. It is still determined on a case by case basis given the syndicate of banks involved in the lending process, so an agreement needs to be formulated between all stakeholders involved.

Currently, the process for both individuals and large-scale landlords can be akin to going through a new credit application evidencing financial distress. While this can enable you to keep your property, it can also put you in a selective box that may take years to recover from. This means higher interest rates, more difficulty refinancing, and reduced access to credit vehicles that would otherwise be available. Additionally, the increased mortgage payments may result in the need to increase the monthly rent, forcing a tenant to pay a higher monthly rate, to move out, or to face negative credit consequences as a result of unpaid dues.

The below is an example of how an individual’s mortgage payment structure would change if opting for a Mortgage Deferral:

|

Interest Rate 5% |

Start of Deferral Period |

End of Deferral Period |

|

Mortgage Balance |

$400,000.00 |

$410,113.00 |

|

Deferral Period |

6 Monthly Payments |

|

|

Payment Amount (monthly principal and interest) |

$3,150.00 |

$3305.50 (+$155.50*) |

|

Remaining Amortization |

15 Years |

14 Years 6 month |

|

Payment Due Date |

April 1st, 2020 (first deferred payment) |

September 1, 2020 (last deferred payment) |

*As shown above a 6-month deferral can lead to an increase of $155.50 per month for the remaining 14.5 years of the mortgage, a total of $4,137 extra in interest.

Financial Aid Programs

Both Federal and Provincial Governments have recognized the tough financial position that many have found themselves in, because of country wide shutdowns. As a result, in true Canadian fashion, they have pledged large sums in order to provide relief for individuals and businesses. The relief measures range from tax credits, increased income benefits, and most importantly, emergency funds for those whose incomes are affected by the virus.

Each province has provided their own form of relief, so we will focus on the Canada Emergency Response Benefit (CERB), which will provide $2,000 a month for up to 4 months during this crisis. Many are criticizing the benefit,

lamenting that they will not be able to live on $2,000 a month, and are still calling for a rental strike – this is especially true in places like Toronto and Vancouver, where landlords have taken advantage of rental demand and raised rents to levels higher than the affordability index; so tenants are paying upwards of 40-50% of their regular income on rent.

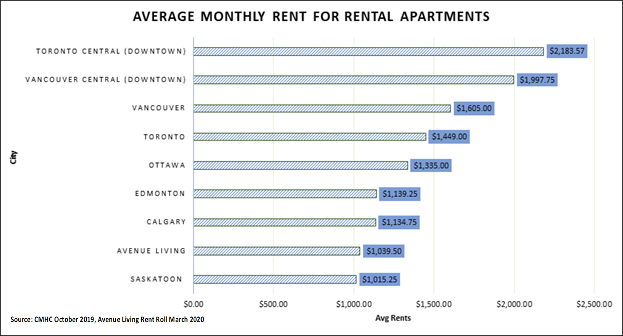

As shown below, rents within Prairie provinces have remained relatively low. In light of the storm, the economic benefits at $2,000 a month demonstrate the fact that the Prairie region and the Avenue Living Portfolio are more affordable places to live and support a continued flight to affordability.

Average of all unit types – primary rental market:

The 30% rent rule is a popular guideline to determine what percentage of income should be allocated towards rent. In Ontario alone, 46% of renters spend more than 30% of their income on rent, while 21% spend more than 50% of their income on rent. This means, during uncertain times, renters might not be able to cover other necessary expenses, such as groceries, paying off debt, or further their financial goals.

Avenue Living understands the harrowing circumstances renters currently face, hence why Avenue Living’s rents are below the national average.

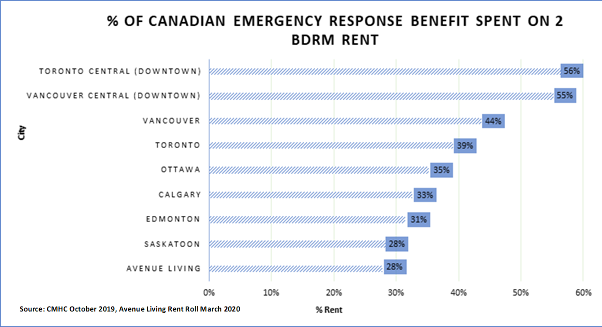

Percentage of $4,000 household income allocated towards a 2-bedroom monthly rent:

Avenue Living’s Solution

Given the precarious situation Canadians are situated in, Avenue Living took the proactive approach of launching a Prairie Relief Team. This Team is mandated to respond to the needs of its 20,000+ residents across its Western Canadian portfolio in a timely manner. The goal is to inform Avenue Living residents of their options, including providing sympathetic solutions to their concerns.

We listen, understand and provide a path that accommodates renters during these turbulent times. The Team has already been instrumental in ensuring that there was a portfolio-wide freeze on rent increases, placing 500 suites at a discounted rate, as well as the introduction of weekly rent options. The weekly (or bi-weekly) rent option matches the frequency of Government aid to provide an easier budgeting tool. For example, we have suites available at $150-250 a week rather trying to save a weekly $500 Government cheque for a large monthly rent payment.

To learn more about the Prairie Relief Team and other initiatives that Avenue Living is taking to ensure everyone in the Prairies has a safe and secure place to live, follow our blog at https://www.avenuelivingam.com/insights/ or reach out at IR-COVID-19@avenueliving.ca.